🗓️ Weekly Quotes: Meta, Paypal, Google, Amazon...

✅ [FREE] Analysing the Earnings Calls of Visa, Pluxee, Paypal, Amazon, Google, Microsoft, Meta, McDonald's, Apple and Roku.

🔥 Founder Offer! 30% off forever!

Upgrade to a paid subscription now and get 30% off forever!

👇 Simple, just use the link below and subscribe using the 30% discount code!👇

🚨 Last hours to take advantage of the discount🚨

🗓️ This week's earnings calendar:

This week has been one of the highlights of Q3 earnings season, with many top-tier companies delivering their results.

Normally we select 8 quality companies but this time we have had to expand to 10 due to the amount of good companies that have presented this days.

The 10 quality picks, as identified by Quality Value, include:

Visa [FREE]: We're kicking things off with a free recap of the earnings call from one of the greatest companies of all time. We'll dive into the results of the oligopoly it forms with Mastercard. Their results are key to understanding the current state of the economy.

Pluxee [FREE]: This Wednesday, we published the latest thesis in Quality Value: Pluxee. On Thursday, they released their Q3 results, so we decided to analyze them and share our opinion for free.

Paypal: Next, we’ll look at the results of a top payment company currently going through a rough patch—are these just tough times, or is a turnaround in sight?

Amazon: Then, we’ll review the results from the e-commerce giant that also holds the largest market share in cloud services.

Google: we consider one of the best companies globally—will it stay on top over the next decade?

Microsoft: Another elite-quality company—are shares overvalued? We'll find out in the results.

Meta: The leading social media platform—is it still the undisputed champion?

McDonald's: Recent restaurant-related infections at McDonald's caused some chaos—has this impacted their results?

Apple: Warren Buffett has been trimming his Apple holdings recently—what could he be seeing? Let’s see if the results offer any clues.

Roku: Finally, we’ll examine a streaming video company that was highly promising during the pandemic—is there still a future here, or was it just hype?"

Let's get straight to the point. 👇

✅ Summary and analysis of earning calls:

1- Visa:

📊 Post-earnings share price performance:

🎬 General summary of the presentation by the Board of Directors:

Strong Financials: Q4 net revenue at $9.6 billion, up 12% YoY; EPS increased by 16%.

Payment Volumes: Global payments volume grew 8% YoY in constant dollars; cross-border volume (ex. intra-Europe) rose 13%; processed transactions up 10%.

Key Business Drivers: Stability in consumer payment volumes; U.S. growth at 5%, international at 10%.

Tokenization & Credentials: Over 4.6 billion credentials issued (+7% YoY) and 11.5 billion tokens with 30% of transactions tokenized.

Merchant Reach: Surpassed 150 million global merchant locations, fueled by events like the Olympics.

Notable Partnerships:

Renewals: Cantaloupe for self-service commerce, AppFolio for rental payments, agreements with major banks like NatWest, and partnerships with fintechs.

B2B Growth: Visa Direct transactions up 38%, with partnerships including JPMorgan Chase (Europe) and Adyen (B2B travel solutions).

New Flows & Innovation:

Visa A2A Launch: Set for 2025 in the U.K., enhancing account-to-account payments.

Fraud Prevention: Visa Protect recognized for fraud innovation; expansion to 10 RTP networks in 2025.

Value-Added Services: Revenue surged 22% YoY, with notable growth in consulting and issuing solutions.

Strategic Investments: Acquisition plans for Featurespace to bolster AI-driven fraud prevention.

2025 Outlook:

Guidance: High single-digit to low double-digit growth expected, with pricing impacts more weighted to the second half.

Expense Management: Adjusted operating expense growth anticipated in high single digits to low double digits.

EPS: Forecasted growth in the high end of low double digits.

Capital Returns: $5.8 billion in stock repurchases in Q4; increased dividend by 13%.

Challenges & Considerations:

Economic Impact: Stability in consumer spending; cautious outlook on Asia Pacific due to macroeconomic headwinds.

Regulatory Concerns: Legal response to DOJ lawsuit over debit market competition.

🎙️ Summary of the questions and answers:

Regulatory & Litigation Landscape:

Visa is actively engaging with regulators worldwide, confident in managing U.S. litigation (e.g., DOJ lawsuit) without disclosing specific revenue exposure to U.S. debit.

Competitive Environment:

Account-to-account (A2A) payments are growing, with Walmart expanding related offerings. Visa is positioned to add value through innovation and strong product differentiation.

Commercial Volumes:

Q4 decline due to days mix; long-term outlook remains optimistic, expecting commercial volumes to outpace consumer growth over time.

AI & Featurespace Acquisition:

AI seen as a dual driver for both operational productivity and enhancing competitive positioning. The acquisition supports fraud prevention efforts globally.

Growth Outlook for FY '25:

Growth across consumer payments, new flows, and value-added services expected to be stable; influenced by incentive renewals, cross-border volumes, and macroeconomic trends.

Open Banking in the U.S.:

New CFPB rules aligned with Visa’s strategy. Tink and open banking solutions offer potential for growth in data aggregation services.

Value-Added Services (VAS) Strategy:

Steady VAS growth through tailored offerings for Visa and non-Visa transactions, leveraging platforms like CyberSource, DPS, and Pismo.

Cross-Border Revenue Dynamics:

Q4 stable at 9% growth; FX volatility and volume mix contributed to results, with expectations for similar trends moving forward.

Early FY '25 Indicators:

October showed a strong start in debit volume, with U.S. growth reflecting day mix effects and lapping of prior Reg II impacts.

Operating Leverage:

Visa remains committed to strategic investment in growth, balancing expense growth with revenue performance for long-term gains.

Market Share & Competitive Wins:

Strong renewal activity highlights Visa's competitive edge and client trust across major global markets, fueling continued business expansion.

📋Links to the investor relations website

2- Pluxee:

📊 Post-earnings share price performance:

🎬 General summary of the presentation by the Board of Directors:

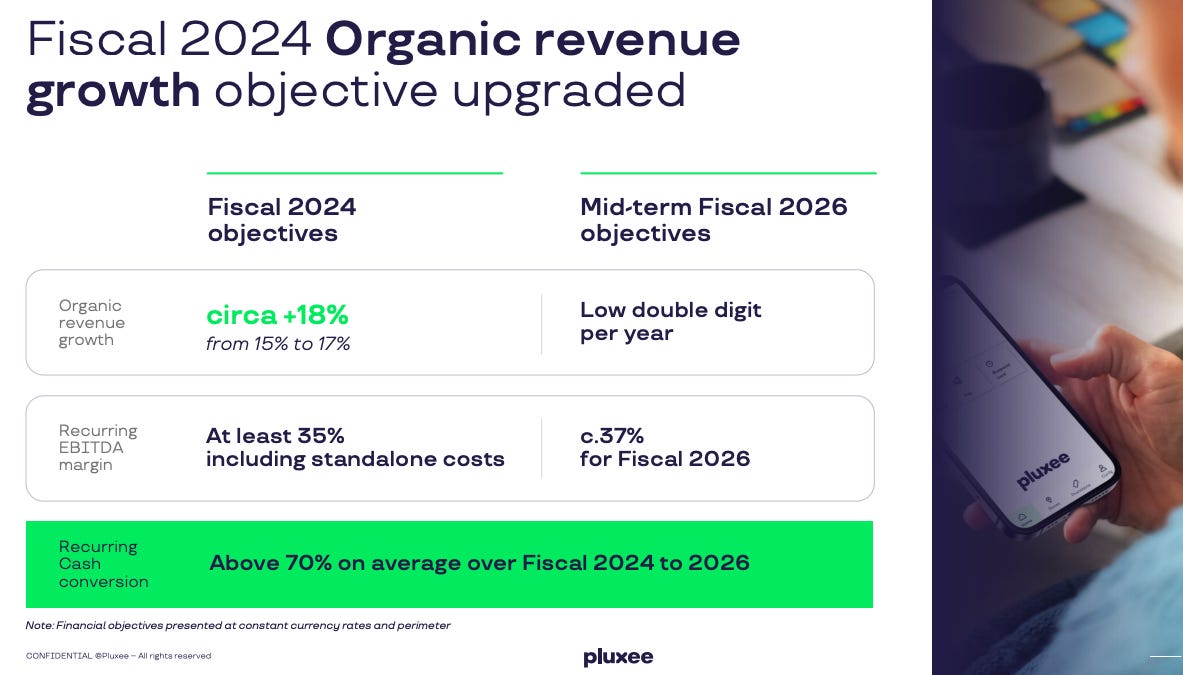

Standalone Success: FY 2024 marked Pluxee's first year as an independent listed entity, demonstrating robust strategic execution, surpassing growth targets, and achieving two guidance upgrades.

Revenue Growth: Total revenues reached €1.210 billion (+18.6% organic growth), primarily driven by a strong 22.5% surge in Employee Benefits, significantly outpacing initial low double-digit growth targets.

EBITDA and Margins: Recurring EBITDA rose to €430 million (+24.8% organically), achieving a 35.6% margin (36.4% organically), up 183 bps—surpassing the stable margin target and realizing over 70% of the 3-year expansion goal.

Cash Conversion: Exceptional free cash flow at €379 million with an 88% conversion rate, well above the 70% target, showcasing effective operational leverage and efficiency.

Dividend Policy: Enhanced shareholder returns with a €0.35 dividend per share based on a 25% payout of adjusted net profit (€203 million), aligning dividends with operational performance.

Outlook for FY 2025/2026: Reaffirmed low double-digit organic revenue growth, targeting a 75 bps annual EBITDA margin increase, and raised cash conversion guidance to over 75%.

Key Strategic Moves: Successful M&A with Santander in Brazil and the acquisition of Cobee in Spain bolstered market positioning and will contribute accretively from FY 2026 onwards.

Regulatory Considerations: A potential 5% cap on Italian merchant commissions factored into forecasts, with proactive adaptation measures planned.

Float Revenue and Interest Rates: FY 2024 float revenue rose 69%, supported by a strong 5.7% yield; future projections account for expected lower rates offset by baseline float growth.

Exceeding Targets: FY 2024 results surpassed all business and financial objectives, showcasing Pluxee's operational strength and strategic execution.

Strategic Positioning: Emphasized resilience amid industry and macroeconomic challenges, leveraging Pluxee’s track record in adaptability and seizing market opportunities.

Structural Growth Confidence: Reinforced belief in the sector's long-term growth potential, supported by a scalable business model poised for strong organic expansion, enhanced operational efficiency, and robust cash flow generation.

Optimistic Guidance: Upgraded financial targets for FY 2025 and 2026, highlighting continued commitment to ambitious growth and profitability.

Execution Focus: Management remains dedicated to precise execution and aims to maintain transparency with the financial community, providing updates on progress in upcoming quarters.

🎙️Summary of the questions and answers:

Capital Allocation & Share Buybacks: Company reaffirmed its commitment to its capital allocation strategy, prioritizing CapEx, targeted M&A, and shareholder returns. Share buybacks not ruled out but currently secondary to M&A opportunities due to stronger potential returns.

Operating EBITDA Margin Decline: FY 2024 saw a 130 basis point decline, attributed to LatAm bad debt, overlapping legacy costs from Sodexo management fees during early standalone ramp-up, and other one-offs. Margin improvement in H2 (+25 bps) demonstrated early operational leverage gains.

Regulatory Landscape in Italy & France: Italian market contribution is under 3% of financials; potential regulatory fee caps noted as minimal risk. Broader regulatory adaptations are considered part of business operations. In France, government discussions around digitization and expanded meal benefit usage continue, with full implementation targeted by 2026.

Growth Projections & Regional Dynamics: Committed to low double-digit organic revenue growth for FY 2025 and 2026, driven by LatAm and Rest of the World amid less favorable conditions in Continental Europe. Growth levers include SME penetration, cross-selling, and face value adjustments.

Float Revenue Strategy: Expected slight organic increase supported by improved balance sheet baseline and optimized cash investment maturities despite anticipated rate decreases.

Chile Contract Update: Ongoing tendering process after disqualification, with potential impact until December; management confident in minimal long-term disruption.

Tech Spend & Take-Up Rates: Transitioning tech investment to OpEx (EUR 173M in FY 2024) due to SaaS-driven specifications, impacting EBITDA margin but offset by operational efficiencies. Take-up rate improvements linked to commercial initiatives and Brazil’s regulatory changes, with stabilization expected going forward.

Overall Outlook: Strong confidence in achieving enhanced EBITDA margins (+75 bps per annum) through scale and efficiency, aligning with strategic growth initiatives and favorable market positioning.

✅ Quality Value Opinion

The results are very positive. Essentially, they have confirmed that they are meeting the 2024 guidance and have also raised the guidance for recurring EBITDA margins by 75 basis points. What we like the most is that they have increased cash conversion from 70% to 75%. If they continue growing at double digits, even at 10%, maintain margins, and improve conversion, cash generation will keep growing year after year. On the other hand, another risk that led to a drop of more than 10% last week was the impact of Italian regulation. In our thesis, where we explained this in detail, we estimated an impact on 3.8% of sales. Ultimately, the company communicated that it would be less than 3%. The impact is minimal and especially at this valuation, but regulatory risk, particularly in Europe, must continue to be monitored. On the negative side, we have capital allocation. They announced a dividend with a 25% payout ratio. In my opinion, given the current stock price, they should have opted to extend and expand the share buyback plan. Overall, solid results and good outlook; we believe they can meet the provided guidance.

📋Links to the investor relations website

3- Paypal:

📊 Post-earnings share price performance:

🎬 General summary of the presentation by the Board of Directors:

From this point, the content is exclusive to paying subscribers. Subscribe now, take advantage of the launch offer, and gain access to all deals.

🚨 Last hours to take advantage of the discount🚨